Global Cleantech Innovation Index - Country Profiles

The country profiles examine countries’ strengths and weaknesses in the 2017 Index. This serves as an important reference for policymakers, entrepreneurs, investors, and industry stakeholders looking to for an overview of specific country performances. For more detail, refer to the Report page.

| A | B | C | D | E | F | G | H | I | J | K | L | M | N | O | P | Q | R | S | T | U | V | W | X | Y | Z |

-

Argentina

Argentina scores below the mean for all metrics. The country places 2nd last in the Global Innovation Index out of the countries measured, but it scores better for perceived entrepreneurial activities and early-stage business activity. Argentina has a very low cleantech R&D budget and lacks financial activity, which accounts for the country's low score for cleantech-specific drivers. Very little evidence for emerging cleantech innovation was recorded, exemplified by the low number of environment-related patents filed. In addition, Argentina does not register any commercialised cleantech innovation to speak of. In this pillar, Argentina ranks last of all countries in the Index for cleantech imports. Neighbouring country Brazil scores higher for most indicators, except in cleantech-specific drivers, where Argentina scores higher.

-

Australia

Australia scores well above the mean for inputs to innovation, but this does not translate into solid outputs. The innovation landscape in Australia is well developed, and Australia scores high across all indicators for the general innovation drivers. Cleantech funds and investors are well represented, and the amount raised by these cleantech funds lies well above the average. However, the public cleantech R&D budget is relatively low. Australia has relatively few environmental patents, which results in an emerging cleantech score that lies below the mean. The country's worst performance is for commercial cleantech, where one of the most telling metrics is its very low amount of cleantech exports.

-

Austria

Austria displays an average overall performance, with its best performance for evidence of commercialised cleantech. The country's ecosystem is well-suited for entrepreneurship, and stands out amongst its neighbours, Germany and Switzerland, for early stage innovation. Austria has a large cleantech R&D budget, but it has mixed results for its attractiveness as an investment market. Despite scoring well above average for its number of patents, Austria is dragged down by its low venture capital investment in the cleantech sector, giving it a score slightly below the mean for emerging cleantech. High levels of international trade in cleantech and a well-established renewable energy sector are hallmarks of Austria's strong commercialised cleantech.

-

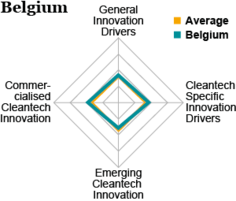

Belgium

Belgium has an all-round average performance, with cleantech-specific drivers and commercialised cleantech slightly above the mean. Belgium's relatively strong score for its general innovation landscape is balanced by low perceived opportunities and early-stage entrepreneurship. For cleantech-specific drivers, Belgium finds itself in the middle of the pack. A highlight is its strong cleantech R&D budget, which is larger than its neighbours, the Netherlands, Germany, and France, when weighted by GDP. The country's evidence of emerging cleantech score is held up by the high percentage of Belgian companies featured in the Global Cleantech 100. Belgium ranks 3rd for cleantech IPOs, behind Singapore and the USA, but it is denied a top score for commercialised cleantech by its proportionally low levels of renewable energy consumption.

-

Brazil

Brazil scores below the mean for all metrics. General innovation drivers are Brazil's strongest performance, with the country scoring very low for general innovation inputs, but ranking 1st for early-stage entrepreneurial activity. Brazil has very limited cleantech-friendly policies and a low R&D score, but the country is an attractive destination for renewable energy investment. Emerging cleantech in Brazil is low, but the country performs better than neighbour Argentina in this particular indicator pillar. Brazil's score for commercialised cleantech is explained by the country's high renewable energy consumption, and the renewable energy jobs that accompany it. However, the country has low cleantech imports and exports, bringing the overall pillar score to below average.

-

Bulgaria

Bulgaria scores below the mean on all metrics. The data show that Bulgaria struggles to convert its inputs to innovation into outputs. For general innovation drivers, there is a strong lack of early entrepreneurial activity, despite the country having a Global Innovation Index score that outperforms neighboring countries like Romania, Greece and Turkey. Bulgaria takes the 4th place overall for the number of cleantech organisations and has recently seen the establishment of Cleantech Bulgaria, a national business network for cleantech innovation. However, the country scores less well for its cleantech R&D budget and its attractiveness as a destination for renewable energy investment. The country did not register any early-stage investment, stymieing emerging cleantech. For commercial cleantech, Bulgaria also did not register any late stage investment, combined with low cleantech exports.

-

Canada

Canada registered a high score overall, coming 4th in the Index, but with especially strong results for emerging cleantech. The country has a strong score in the Global Innovation Index, but what truly distinguishes it is its score for early entrepreneurship, which is 2nd overall. For cleantech-specific drivers, Canada scores high for the number of cleantech funds, and even ranks 1st for the amount of funding available. However, there are only a few cleantech organisations and clusters. The country is a joint top-scorer for the amount of venture capital investment, together with three other countries in the Index, while also having many companies in the Global Cleantech 100. Late-stage investment is well established in Canada, with the country ranking high for public cleantech companies and M&A activity, leading to a strong score for evidence of commercialised cleantech.

-

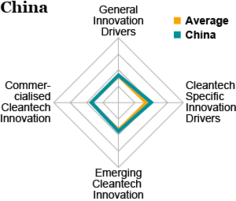

China

China has a stable performance, registering close to the mean for all metrics. The country scores quite high for early-stage entrepreneurship, despite low perceived opportunities. For cleantech-specific drivers, the country is a favourite investment destination for renewable energy investment, coming in 2nd place after the US. It lags behind for cleantech investors when viewed globally, even though the country scores highest amongst its Asian neighbours. China performs strongly for early-stage venture capital investment but ranks lower for cleantech patents, giving it a score close to the mean for emerging cleantech. For commercialised cleantech, China scores consistently in the middle of the pack, with no particular deviations from the average.

-

Czech Republic

The Czech Republic scores below the mean in all four pillars. For general innovation drivers, the generally favourable entrepreneurial environment is not translated into a strong entrepreneurial culture, with perceived opportunities and early entrepreneurship that only match the Eastern European average. The country has a low attractiveness for renewable energy investment and an underdeveloped private cleantech investment scene, resulting in a cleantech-specific drivers score that lies well below the mean. This is also reflected in low early-stage venture capital investment that, combined with a low cleantech patent score, leads to the Czech Republic being located on the lower end of the spectrum for this emerging cleantech pillar and the Index generally. For commercialised cleantech, the Czech Republic has high cleantech imports that stand out among its neighbouring countries, Austria and Poland.

-

Denmark

Denmark is the top scorer for this edition of the GCII. The country scores above the mean for all metrics, but is especially strong in commercialised cleantech. Denmark takes the 8th place in the Global Innovation Index, and performs on the Nordic average for perceived entrepreneurial opportunities and early-stage entrepreneurial activity. The country is the top performer for the amount raised by cleantech funds (sharing its position with Israel) and the number of cleantech organisations, making Denmark the top performer for cleantech-specific drivers. As previously mentioned in this report, a recent cut (of around 50%) in the public cleantech R&D budget is not accounted for in the 2017 Index, and is likely to have a detrimental effect on Denmark's ranking in this indicator in future. For emerging cleantech, the country is 4th in the ranking for patents, but the low amount of venture capital investment pushes Denmark down to 11th place in this pillar. Commercialised cleantech is Denmark's strong point, with the country scoring top marks for cleantech exports, the number of public cleantech companies and the number of renewable energy jobs, which when combined put Denmark in 1st place.

-

Finland

Finland reaffirms its reputation as a cleantech leader, scoring above the mean for all metrics. While Finland ranks well on the Global Innovation Index, placing 5th overall, it doesn't score as high as its Nordic neighbours for perceived opportunities and early-stage activity. For cleantech-specific drivers, Finland takes the 2nd place overall, with strong performances for its cleantech R&D budget and the number of cleantech funds present. It is not, however, attractive for renewable energy investment, where only Indonesia, Russia and Greece score lower. Emerging cleantech is Finland's strong point, with strong performances across all indicators. For evidence of commercialized cleantech, Finland's performance is nuanced, with a strong showing for renewable energy jobs and M&A activity, but relatively low cleantech imports and exports.

-

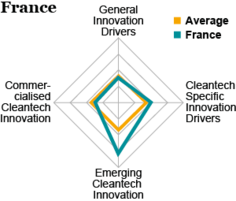

France

France scores around the mean for most metrics, with a strong showing for emerging cleantech. The country has a Global Innovation Index score that is lower than Germany, but higher than Belgium. However, it scores quite low for perceived entrepreneurial opportunities and early-stage business activity. For cleantech-specific drivers, the country scores slightly higher than the mean. This is explained by an average showing for all data points, with the country's recent issuing of 7.5 billion euro green bonds promising further cleantech commitment. Emerging cleantech in France is strong, backed by the high amount of early-stage venture capital investment in the domestic cleantech sector. Commercialised cleantech lies slightly below the mean, despite France taking a shared 1st place for cleantech IPOs. Factors explaining the lower score for commercialised cleantech include the low renewable energy consumption and relatively low cleantech commodity import and export figures.

-

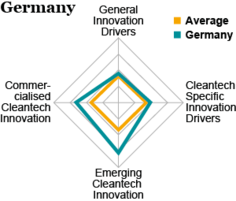

Germany

Germany scores above the mean for all metrics, but is especially strong in outputs of innovation. While Germany scores strong for the Global Innovation Index it has very low evidence of early-stage entrepreneurial activity, coming in second-to-last place, just ahead of Italy. For cleantech-specific drivers, Germany is very attractive for renewable energy investment, but it is being held back by the lack of a presence of private investors. The country's score for emerging cleantech is supported by its top score for environmental patents. Germany's strong cleantech import and (especially) export figures, as well as the high number of renewable energy jobs are the basis of its strong commercialised cleantechscore.

-

Greece

Greece scores well below the mean on metrics. Despite a score in the Global Innovation Index that is higher than Russia or India, Greece puts down the lowest score for perceived opportunities and also ranks low for early-stage activity. The cleantech-specific drivers are stymied by Greece's unattractiveness as a destination for renewable energy investment (the country takes last place), but its cleantech R&D budget, although quite low on a global scale, is still higher than that of Bulgaria and Romania. Emerging cleantech in Greece is low. The country has no Global Cleantech 100 companies. Venture capital investment, and cleantech patent activity also rank low. Commercialised cleantech in Greece suffers from an underdeveloped investment environment, with no private equity, M&A, or IPO activity to speak of.

-

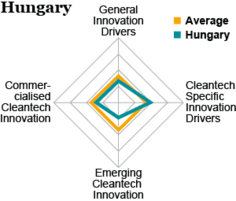

Hungary

Hungary scores slightly below the mean for general innovation drivers and commercialised innovation. Cleantech-specific drivers are Hungary's strong point, while emerging cleantech is lagging behind. For general innovation drivers, Hungary puts down an average performance, both for government policies regarding entrepreneurship and the public perceptions of entrepreneurship. Hungary is ranked 1st amongst the countries surveyed for cleantech R&D, and it has a high number of cleantech organisations. However, the country is not very attractive as a renewable energy investment destination. Despite bettering many of its neighbouring countries for emerging cleantech, Hungary lags behind on a global scale. For commercialised cleantech, the country is faced with an underdeveloped investment environment.

-

India

India scores below the mean on all metrics, except for a strong performance in cleantech-specific innovation drivers. While India's score on the Global Innovation Index is low, the public seems to have a positive view of entrepreneurship, with relatively high scores for perceived opportunity and early-stage entrepreneurial activity. India's performance for cleantech-specific innovation drivers is explained primarily by its attractiveness as a renewable energy investment destination (coming 3rd). However, the country scores low marks for its cleantech R&D budget and the presence of cleantech organisations and clusters. Evidence of emerging cleantech innovation in India is quite low, mainly because of a relatively low amount of early-stage venture capital investment. The country's low performance in showing evidence of commercialised cleantech is due to a combination of little late-stage private investment, low cleantech exports, and a relative weakness in renewable energy jobs relative to India's total work force, which is likely to change with the country's expanding renewable energy sector.

-

Indonesia

Indonesia scores well below the mean for metrics, and the country shows little sign of commercialising the low inputs to innovation scores into innovation outputs. With regard to general innovation drivers, Indonesia has the lowest Global Innovation Index ranking of all countries, but this is not reflected in the country's perceptions to innovation and its strong early-stage entrepreneurial activity. Cleantech-specific drivers are low as well, with Indonesia having the second-lowest cleantech R&D budget and the third-lowest country attractiveness for renewable energy. Indonesia did not register any emerging cleantech, coming last for every single metric. There is little evidence for commercialised cleantech, with the country registering low cleantech import and export numbers, in particular.

-

Ireland

Ireland puts down high marks for general innovation drivers and emerging cleantech innovation, while performing around the mean for cleantech-specific drivers and commercialised cleantech. Ireland scores high for the Global Innovation Index, and puts down reasonable scores for early-entrepreneurship and perceived opportunities. With regard to cleantech-specific drivers, Ireland is the top scorer for the number of cleantech funds and has a high number of cleantech organisations, but this does not translate into a top score for the amount raised in cleantech funds. The country has high levels of early-stage venture capital investment, but a small number of patents lowers the country's overall score for emerging cleantech innovation. In commercialised cleantech, Ireland is the top scorer for M&A activity, but has low levels cleantech imports and exports.

-

Israel

Israel, the champion of the 2014 GCII, scores above the mean for every metric. The country scores relatively high for perceived opportunities for entrepreneurship, while also registering a good score in the Global Innovation Index. Israel scores strongly in investment indicators in cleantech-specific drivers, ranking 1st for the number of cleantech funds and cleantech investors, and the amount raised by these funds, but the country lacks attractiveness as a renewable energy investment destination. Israel's score for emerging cleantech is explained by its top scores for the amount of venture capital investment and the presence of Israeli companies in the Global Cleantech 100. With regard to commercialised cleantech, Israel has high M&A and IPO numbers, but it has low renewable energy consumption.

-

Italy

Italy generally scores below the mean, except for cleantech-specific innovation drivers. Italy's score for the Global Innovation Index is quite low, and this is further compounded by the country's last place overall for early-stage entrepreneurship. While Italy has many cleantech-friendly government policies, an underdeveloped early-investment landscape drags Italy's cleantech-specific drivers score down. Emerging cleantech in Italy is quite low, and this is mainly due to low venture capital investment. For the presence of companies in the Global Cleantech 100, the country scores higher than fellow Southern European countries, Greece and Portugal, but lower than Spain. The commercialised cleantech innovation score is mixed, with Italy leading other Southern European countries in M&A activity, but lagging behind them for the number of public cleantech companies included in cleantech indices.

-

Japan

Japan is the 2nd highest ranked Asian country, after South Korea. It scores above the average across both inputs to and outputs of cleantech innovation, with a particular strength in emerging cleantech. For general innovation drivers, Japan scores slightly above the average. The country has low perceived opportunities for entrepreneurship, and Japanese culture is traditionally risk-averse. Japan is ranked 14th for cleantech-specific drivers and shows a mixed performance. While the country has a relatively high cleantech R&D budget and a high renewable investment attractiveness, there are very few cleantech funds and investors active in the country. For emerging cleantech, Japan ranks 3rd for cleantech-related patent filing, indicating an active and successful cleantech research sphere. However, Japan ranked 1st for patents in the 2014 GCII report, showing a relative decrease in patent activity. Commercialised cleantech shows a mixed picture. Both early- and late-stage financing relative to Japan's size of economy is lagging behind the majority of other Index countries, and there are only a few Japanese companies included in cleantech publically traded indices. However, Japan has high levels of cleantech imports and exports.

-

Mexico

Mexico scores below average in both inputs to and outputs of cleantech innovation, occupying the 32nd rank in the GCII. The country displays a below-average score for general innovation drivers, mirroring its score for cleantech-specific drivers of innovation. Weaknesses in this pillar include public cleantech R&D expenditure, as well as access to private finance, and a lack of cleantech organization/cluster establishments. Thus, there is a general failure to promote the growth of the cleantech innovation ecosystem, illustrated in the 36th rank for emerging cleantech innovation. Mexico's relative strength lies in commercialised cleantech, scoring close to the Index average. This strength can in part be attributed to Mexico's high cleantech commodity trade activity, scoring 4th place for imports, which is fueled by new policy and market instruments aimed at meeting the country's renewable energy goals. The Mexican outputs to innovation seem to be limited, however, by the lack of significant late-stage financing and limited strategic cleantech road-maps.

-

Netherlands

The Netherlands scores above the global average in both inputs to and outputs of cleantech innovation, achieving the 15th rank in the overall Index. Scoring 5th in general innovation drivers, the Netherlands succeeds in producing a high-quality innovation ecosystem, and promotes a strong national entrepreneurial culture. Above average access to private finance for start-ups together with a good score for public R&D expenditure in the cleantech sector provides the country with significant cleantech-specific drivers.. This manifests in the country's good score for emerging cleantech, scoring 11th place for evidence of early-stage venture capital investment. Thies culminates in the Netherlands' relative success in commercialised cleantech, particularly in its strength in cleantech trade, scoring 3rd and 6th place in cleantech commodity imports and exports respectively. A weakness, however, is its low renewable energy consumption relative to total primary consumption.

-

New Zealand

New Zealand shows a mixed performance across inputs to and outputs of cleantech innovation, and occupies the 21st rank in the overall Index. It performs above average for general innovation drivers, indicating that the overall national innovation ecosystem is streamlined and entrepreneurial culture supported. However, cleantech-specific drivers are lagging behind â illustrated by particular weaknesses in cleantech-supportive government policies and low public R&D expenditure to the cleantech sector. This lack of government support as well as limited private early-stage financing translates into New Zealand's low 28th place in emerging cleantech. Despite this, the country scored above global-average for commercialised cleantech. This is attributed to its 3rd place in the renewable energy consumption indicator, providing a proxy for clean energy technology, and related clean energy jobs.

-

Norway

Norway performs above the global-average in both inputs to and outputs of cleantech innovation, with a particular strength in producing cleantech-specific drivers. While the overall score for general innovation drivers remains above average, Norway shows a relatively low score for total early-stage entrepreneurial activity, indicating that the good innovation support frameworks do not directly translate into a large proportion of the population starting a business. Norway's strength lies in promoting cleantech-specific drivers of innovation, ranking 2nd in this pillar with top performance in public R&D expenditure to the cleantech sector. For evidence of emerging cleantech, Norway scores just above the global-average, with a relative weakness in cleantech-related patent filings as evidence for new innovations. Norway's success in commercialised cleantech is reflected in its top score for number of late-stage private equity investments in cleantech, as well as a high share of renewable energy consumption, although the latter relates mainly to old hydropower assets rather than a strong uptake of modern renewable power which is also clear in this Index from the low score in renewable energy investment attractiveness.

-

Poland

Poland ranks 24th in the GCII, only beating the global-average in cleantech-specific drivers. A weakness in its general innovation drivers indicates that the Polish innovation ecosystem requires streamlining and support. Poland's strength in cleantech-specific drivers can be attributed to a top score in cleantech-supportive governmental policies, and above average scores for access to private funds, as well as public R&D expenditure. The weak score in emerging cleantech, ranking Poland at 24th place for this index pillar, can be explained by the complete absence of early-stage venture capital investment into the cleantech sector and no companies making the GCT100 list in the last 3 years. Nevertheless, Poland's cleantech-related patent filing scores at global-average. Commercialised cleantech highlights strong national cleantech commodity demand through Poland's high import score. Low late-stage investment in Polish cleantech companies, as well as below-average evidence of renewable energy consumption and employment, highlight the country's areas for improvement.

-

Portugal

Portugal scores below the global-average in both inputs to and outputs of cleantech innovation, scoring 27th place in the overall Index. The country lacks a strong entrepreneurial culture and also a streamlined innovation ecosystem, resulting in a low score for general innovation drivers. Success in cleantech-specific drivers is limited by a small public R&D budget allocated to cleantech, and very limited cleantech start-up access to private capital. However, the presence of cleantech clusters and organisations, as well as the above average cleantech-supporting government policy score, are relative strengths for Portugal. Evidence for emerging cleantech innovation scores put Portugal in a low 33rd place, the country's weakest across the four pillars measured. Portugal shows mixed performance in commercialised cleantech resulting in a 24th place in this pillar. While the country shows above average evidence of renewable energy consumption and related energy jobs, this strength is outweighed by the absence of late-stage private finance and activity in cleantech commodity trade. Portugal's overall performance lies well below the average for all European countries analysed.

-

Romania

Romania scores below average for both inputs to and outputs of innovation, ranking 35th overall in the Index. A low score for general innovation drivers indicates that the country is lacking necessary support structures, education and policy to build a strong entrepreneurial environment. Romania ranks lowest among all European countries for cleantech-specific drivers, highlighting a particular weakness that inhibits emerging cleantech innovation. No evidence of early-stage funding was recorded, and little measure of successful cleantech start-ups exists, but Romania's score for cleantech patents reaches 28th place, above neighbouring Bulgaria. A total lack of observed late-stage cleantech financing and very low scores for cleantech commodity trade set Romania's commercialised cleantech innovation score low. However, the country shows a relative strength in the proportion of renewable energy consumption by total primary consumption (ranking 11th), highlighting the establishment of clean energy technology in the country.

-

Russia

Russia ranks second-to-last in the GCII, with both input to and outputs of innovation well below global-average. The country lacks a strong entrepreneurial culture, as well as a streamlined support structure for the general national innovation ecosystem. The country's weaknesses in cleantech-specific innovation drivers are especially shown in a regulatory system unsupportive of cleantech innovation, an absence of cleantech specific industrial clusters and the lack of any private native cleantech investors. Russia's strength, which is still below global average, lies in providing evidence of emerging cleantech innovation â ranking 27th. A lack of successful start-ups is countered by Russia's small amount of venture capital financing, and an indication of strong cleantech research and intellectual property protection, with 1279 patents filed under cleantech-related technologies in 2013. This, however, does not translate into any significant commercialised cleantech in Russia, evidenced by a lack of cleantech trade activity and late-stage investment. The country nevertheless shows a relative strength in clean energy jobs.

-

Saudi Arabia

Saudi Arabia occupies the 37th place in the Index. The only representative from the Arabian peninsular shows a unique spread of scores between the four indicator pillars. Saudi Arabia scores above average for general innovation drivers, occupying the top rank for the indicator of perceived entrepreneurial opportunities. This indicates that the country succeeds in streamlining the innovation ecosystem, having support and incentives in place to build a strong entrepreneurial culture. However, this does not translate into innovation support to the cleantech sphere in any way, highlighted by Saudi Arabia scoring last in cleantech-specific drivers. This strong contrast is mirrored in the performance in outputs of cleantech innovation, scoring second-to-last. Particular weaknesses are the lack of cleantech research, represented by low scores for cleantech-related patents relative to GDP; very low level of private early- and late-stage financing; low cleantech trade activity; and also low renewable energy consumption. Saudi Arabia's data demonstrates that the lack of national emphasis on cleantech-specific drivers inhibits the establishment and growth of a cleantech innovation ecosystem. However, in its recently unveiled project, Vision 2030, Saudi Arabia outlines the goal to construct a renewable energy capacity of 9.5 GW by 2030, or 10% of the Saudi electricity demand. Although this target is not overly ambitious, it could provide the necessary impetus for the Saudi economy to develop some cleantech innovation outputs and become a more efficient innovator in the field of cleantech.

-

Singapore

Singapore occupies the 14th rank in the GCII, showing a mixed performance across inputs to and outputs of cleantech innovation. While the country scores well above average in general innovation drivers, it does not uphold its high rank in cleantech-specific drivers, ranking only 29th. This indicates that while the country successfully promotes an overall streamlined innovation ecosystem, it lacks focus in the cleantech sphere â with particular areas requiring improving being cleantech-supportive policy and access to cleantech focused funds. Singapore's emerging cleantech scores above average, with a strong score for available early-stage private capital, and a relative weakness in the number of cleantech-related patents filed in 2013. The country places 2nd for commercialised cleantech, with top scores in cleantech commodity trade and a good number of cleantech company IPOs and M&A activity. Whilst partly attributed to the country's limited natural resources and size, Singapore's weakness for this pillar is its renewable energy consumption and related jobs.

-

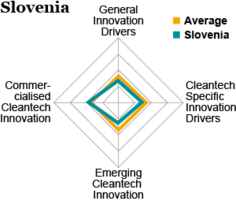

Slovenia

Slovenia occupies the 21st rank in the GCII, but scores below the global-average in general innovation drivers, cleantech specific drivers, and emerging cleantech. Scoring just below Bulgaria for general innovation drivers, Slovenia still has great potential to improve its innovation ecosystem and embedded national entrepreneurial culture. Slovenia shows a mixed performance of cleantech-specific innovation drivers Whilst the country yields a top score for cleantech industrial cluster development and scores well for cleantech supportive government policy, the total lack of start-up access to private finance and low renewable energy investment attractiveness of the country outweigh the relative strengths. This translates to low emerging cleantech, with a particular weakness again being the lack of evidence for early-stage financing in the cleantech sector. Despite these weaknesses, Slovenia manages to score 16th place in commercialised innovation, with strong cleantech commodity exports and imports, but no strength in late-stage private finance indicators.

-

South Africa

South Africa scores below the global average in both inputs to and outputs of cleantech innovation, ranking 31st in the overall Index. The only Sub-Saharan Africa country representative ranks 4th to last for general innovation drivers, indicating that the country lacks a streamlined innovation pipeline and a good entrepreneurial culture. South Africa's relative strength, yet still below global-average, lies in cleantech-specific drivers with a good amount of cleantech-friendly government policy. The country lacks evidence of emerging cleantech, especially shown in the low number of filed cleantech-related patents and low showing of successful cleantech start-ups, despite some early-stage venture capital deployed in the sector. The country scores very low for commercialised cleantech, despite a decent amount of cleantech imports, due to lack of evidence of any late-stage private finance activity, a low score for cleantech commodity exports, and low renewable energy consumption and related employment.

-

Korea Republic

South Korea scores highest amongst all Asian countries in the Index, occupying the 11th rank overall, with a particular strength in outputs of cleantech innovation. The country's performance in general innovation drivers is just above the global average, indicating a relatively streamlined innovation pipeline, but not necessarily a widely embedded national entrepreneurial culture. The score for cleantech-specific drivers lies slightly below the global average, attributable to weaknesses in access to private finance and low numbers of industrial cleantech clusters, despite the relative strength in public R&D expenditure on the cleantech sector. South Korea's outputs of cleantech innovation are, however, well above average. While South Korea ranks top for cleantech-related patents, it lags behind in early-stage finance and successful start-up indicators, ranking 10th place for emerging cleantech. South Korea shows significant success in the commercialised cleantech, with its export and import of cleantech-related commodities ranking 2nd highest overall, only after Singapore. This top performance is contrasted by South Koreas continued lack of late-stage financing in the cleantech sector, or significant shares of renewables in the national energy mix.

-

Spain

Spain ranks 25th in the Index, with a relative strength in evidence of commercialised cleantech. Inputs to innovation score both below the global average and below its smaller European neighbour, Portugal. Particular weaknesses in cleantech-specific drivers are the limited start-up access to cleantech funds and a lack of a cleantech-supportive policy environment, and low R&D expenditure on cleantech, especially compared to other European nations. Failure to show successful emerging cleantech is shown by the low number of successful Spanish cleantech start-ups. Yet, Spain's commercialised cleantech ranks 19th. The country shows evidence of late stage private equity deals, some successful public listed cleantech companies, strong exports of cleantech commodities, and an above average renewable energy consumption. Spain's clean energy related jobs, however, lie below the global average. Another relative weakness lies in Spain's very low cleantech commodity imports.

-

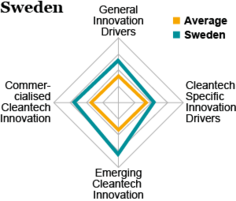

Sweden

Sweden scores 3rd in the Index, trailing its two Nordic neighbours, Denmark and Finland. For general innovation drivers, Sweden shows a particular strength in its citizen's perceived entrepreneurial opportunities, ranking 2nd behind Saudi Arabia. Highlights in Sweden's cleantech-specific drivers are the high public R&D expenditure in the cleantech sphere, evidence for a cleantech-friendly policy environment, and a large number of domestic private cleantech investors. Evidence for emerging cleantech in Sweden is shown by the country achieving the top score in the successful cleantech start-ups indicator, and filing 1.5 times the global average number of cleantech-related patents by GDP. Sweden's commercialised cleantech ranks 3rd overall, with particular national strengths in renewable energy consumption by total primary energy, a proxy for clean energy technology deployment, and related clean energy jobs. The country also scores the top rank for the number of cleantech company IPOs in the last 3 years, when weighted by GDP.

-

Switzerland

Switzerland ranks 10th place in the Index, with an even performance across all indicator pillars above the global average. For general innovation drivers the country scores the 5th place, with a top score in the Global Innovation Index, but lagging behind in indicators of entrepreneurial culture. This indicates that while the national innovation pipeline is supported by policy, education, and finance, it does not yet translate into a high level of actual entrepreneurial activity among the Swiss population. For cleantech-specific drivers, Switzerland's strengths lie in high government cleantech R&D expenditure and cleantech-supportive policy, whilst the country's weaknesses lie in its number of cleantech industrial clusters and below-average score for renewable energy investment attractiveness. Switzerland's performance in emerging cleantech is consistently above average for all indicators, covering early-stage venture capital investment to cleantech-related patent filings. This consistency does not translate to indicators of commercialised cleantech. Switzerland scores high in its share of renewable energy consumption and level of late-stage equity and M&A activity within the cleantech sector, but shows weaknesses in producing publicly listed cleantech companies, the related number of IPOs, and a very low level of cleantech commodity exports/GDP.

-

Turkey

Turkey ranks 33rd in the Index. The country's clear strength lies within general innovation drivers, scoring high in entrepreneurial culture indicators and giving evidence of an active early-stage ecosystem. For cleantech-specific drivers, Turkey lacks strength across all constituent indicators, from a cleantech-supportive policy environment to access to private finance. This reflects in Turkey scoring 3rd to last for evidence of emerging cleantech, with even Saudi Arabia surpassing it. Whilst still well under the global average, the country shows some evidence for commercialised cleantech, mainly attributable to its cleantech commodity imports and above-average share of renewable energy consumption of its total primary energy.

-

United Kingdom

The United Kingdom ranks 7th in the Index, with the highest European country score, excluding the Nordics. The UK yields high scores for all general innovation drivers, except early-stage activity measurements, which is on the lower end of the indicator distribution. For cleantech-specific drivers, the country shows strength in start-up access to private finance, and a relative weakness for government R&D expenditure on the cleantech sector. The UK performs best in evidence of emerging cleantech, ranking 5th, partly attributable to its top score in early-stage venture capital investment activity and a high number of successful start-ups. For commercialised cleantech, the UK lags behind the global average in producing cleantech commodity exports and renewable energy consumption, but shows strength in late-stage financing activity, scoring top in a measurement of cleantech company IPOs.

-

United States

The USA upholds a leading rank in the Index, placing 5th after three Nordic countries and its neighbour, Canada. High scores for general innovation drivers point to the streamlined national innovation pipeline and strong entrepreneurial culture in the USA. For cleantech-specific drivers, the USA shows strengths in start-up access to private finance and scores top for renewable energy investment attractiveness, but has potential to improve in providing a cleantech-supportive policy environment and R&D expenditure on cleantech relative to its GDP. The USA ranks 3rd for emerging cleantech, performing well across all indicators and scoring top for early-stage financing activity. The US also shows evidence of commercialised cleantech with a top position in late-stage cleantech financing through private equity, M&As, and IPOs, as well as a good and growing number of renewable energy jobs. However, the total share of US renewable energy consumption and cleantech commodity exports are lower than global average, and these two indicators brings the score down.